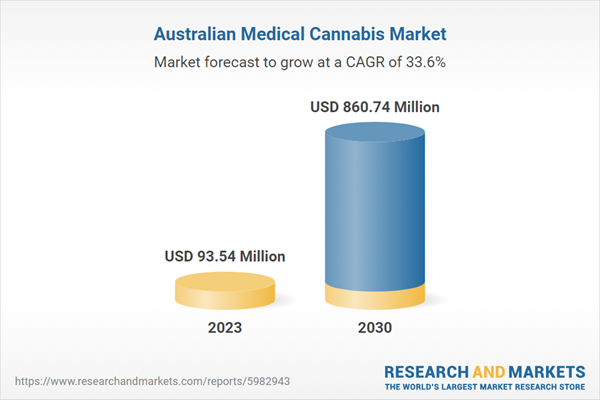

The Australia medical cannabis market size is anticipated to reach USD 860.74 million by 2030 and is growing at a CAGR of 33.6% from 2024 to 2030

The market growth is driven by rising public awareness of the health advantages associated with cannabis consumption. The expanding legalization of marijuana, especially for medical purposes, is expected to significantly contribute to the market growth in Australia.

For instance, in October 2023, the Australian Capital Territory (ACT) introduced certain regulations on the use of cannabis. It stated that individuals aged over 18 can own fresh cannabis up to 150 grams or dried cannabis up to 50 grams. Moreover, several factors, such as the growing legalization of cannabis, expanding patient pool, increasing government initiatives, and the active participation of both domestic & international players in the country, are fueling market growth.

The easing of regulatory restrictions on medical cannabis has created a more favorable environment for the expansion of the market. Regulatory agencies, such as the Therapeutic Goods Administration (TGA), have simplified the approval procedures for medicinal cannabis products, enhancing patient access to these treatments. According to the Australian Journal of General Practice, as of 2021, over 130,000 medicinal cannabis approvals have been granted in Australia, with the majority being issued by general practitioners. Notably, around 65% of these approvals were for the treatment of chronic non-cancer pain. Furthermore, the authorization of medical cannabis use in various Australian states has significantly improved market conditions, facilitating greater production, distribution, and usage of medicinal cannabis products.

Moreover, the presence of a diverse range of industry stakeholders, including both domestic and international players, has contributed to the dynamism of the market. Established pharmaceutical companies, cannabis cultivators, research institutions, and startups are actively investing in the sector, driving innovation and market competition.

This competitive landscape not only fosters product development and innovation but also helps to drive down prices, making medical cannabis more accessible to patients across Australia. For instance, in January 2024, Cronos Group Inc. announced its entry into the Australia market by commencing the delivery of cannabis flowers to Vitura Health Limited. Due to around 10% of Vitura’s common shares, formerly known as Cronos Australia, Cronos would be the cannabis supplier for Vitura. As a result, the market is experiencing sustained growth, with promising prospects for the future.

Australia Medical Cannabis Market Report Highlights

- Hemp dominated the source segment of the market in 2023 due to rising incidences of conditions such as epilepsy and various sleep disorders, alongside increased consumption of hemp-derived products, including hemp CBD and supplements, renowned for their numerous health benefits, are further driving the market

- The chronic pain segment held the largest share, driven by the increasing demand for alternative treatments. Medical cannabis products, particularly THC-rich products, are being recognized as a potential solution for managing chronic pain

- CBD dominated the derivatives segment with a share in 2023. The growth in this market is linked to the legalization of low-dose CBD products by the Therapeutic Goods Administration (TGA). Despite this legalization, these products are still pending approval by the Australian Register of Therapeutic Goods (ARTG)

- Key players operating in the market are focusing on technologically advanced devices that offer users comfort. New product development and strategic alliances, including partnership agreements, promotional activities, and acquisitions, keep market rivalry high

Companies Featured

- Cann Group Limited

- Zelira Therapeutics

- AusCann Group Holdings Ltd.

- Bod Australia

- Althea Group

- ECOFIBRE

- Botanix Pharmaceuticals

- EPSILON

- Little Green Pharma

- Incannex

- Bod Australia

- Cann Group Limited

- ECOFIBRE